Consumer prices rose 0.5% month-over-month in May

What the May 2026 CPI Report Means for Rental Housing

What Happened: Consumer prices rose 0.5% month-over-month in May, according to the Bureau of Labor Statistics, easing slightly from a 0.6% gain in April. On a 12-month basis, the all-items index climbed to 4.2%, the highest annual rate since April 2023 and up from 3.8% in April.

Energy led all increases, rising 3.9% during the month and accounting for more than 60% of the monthly increase in headline CPI. The Gasoline index rose 7.0% month-over-month and is now up 40.5% over the past 12 months. Overall energy prices are up 23.5% over the past 12 months.

Core-CPI rose just 0.25% in May, decelerating from 0.4% in April and matching January and February’s pace.

On an annual basis, core came in at 2.9%, up 10 basis points from April’s 2.8%. Services less energy services rose 0.3% for the month, while shelter and owners’ equivalent rent each rose 0.3%. Rent of primary residence came in at 0.4%.

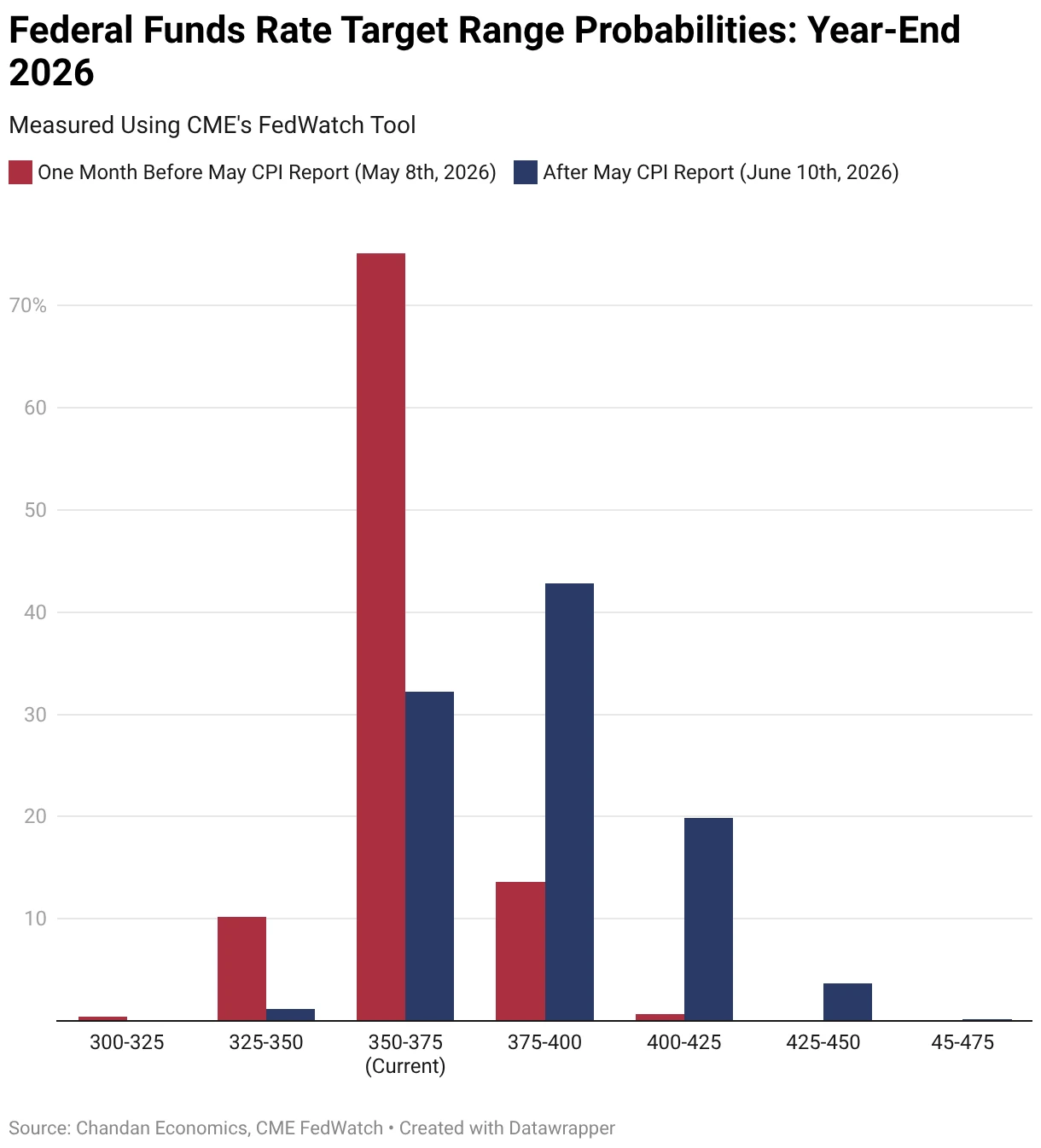

What It Means for Interest Rates: A June interest rate hold remains the overlwhelmingly likely outcome. With monthly CPI landing in line with expectations, there was virtually no change in federal funds rate futures between before and after the report.

After surging sharply following last Friday’s blowout jobs report, U.S. Treasury yields had a largely muted reaction to Wednesday’s CPI data. The yield on the 2-year US Treasury fell slightly after the report’s release, offering some modest relief on short-term borrowing rates. Nonetheless, treasury yields, on average, continue to hover around an annual high as bond markets grow more hawkish about the path of rates and risk.

According to the Chicago Mercantile Exchange’s FedWatch Tool, the odds of an interest rate hike have increased significantly over the past month.

As of the morning of June 10th, directly following the CPI report release, there is a 66.6% probability of at least one 25-basis-point hike by the end of 2026. One month ago, futures markets priced in a meager 14.4% chance of a 2026 rate hike.

Get a Free Multifamily Loan Quote

Access Non-Recourse, 10+ Year Fixed, 30-Year Amortization

What It Means for Real Estate: The upcoming rate environment appears restrictive. At 4.52%, the 10-year keeps debt costs elevated enough that acquisition spreads remain thin and new development is difficult to underwrite to target returns in many markets. These targets require rates to fall, which the market is no longer expecting.

Energy and food inflation above 20% and 3%, respectively, are squeezing renter budgets at the lower end of the income distribution. According to Chandan Economics ‘ May rent collections report, on-time rent collections have been improving but remain 48 basis points below year-ago levels. Recent energy spikes could put upcoming collection rates under pressure.

Shelter CPI’s uptick to 3.4% annually reflects a BLS measurement lag, not a new deterioration in the market. Market-rate rents have stabilized across most metros following the 2024–2025 supply surge, and CPI is catching up to conditions that operators have already absorbed.

How the May CPI Report Shifted Interest Rate Expectations

Market-implied probabilities and Treasury yields before and after the CPI release

| Near-term | Chance of lower rates at next Fed meeting (6/17) | 0.80% | 3.80% | 3.0 ppts |

| Near-term | Chance of higher rates at next Fed meeting (6/17) | 0.00% | 0.00% | No Change |

| Longer-run | Chance of lower rates by year-end 2026 | 0.30% | 1.20% | 0.9 ppts |

| Longer-run | Chance of higher rates by year-end 2026 | 68.30% | 66.00% | –2.3 ppts |

| Longer-run | Chance of lower rates by June 2027 | 0.10% | 0.60% | 0.5 ppts |

| Longer-run | Chance of higher rates by June 2027 | 83.60% | 81.80% | –1.8 ppts |

| Market pricing | Market-implied Fed funds rate: year-end 2026 | 3.88% | 3.88% | No Change |

| Market pricing | Market-implied Fed funds rate: June 2027 | 3.88% | 3.88% | No Change |

| Market pricing | 10-year Treasury yield | 4.53% | 4.52% | –1 bp |

Accessibility

Accessibility